Financial modelling – the next step in EITI reconciliations?

Financial modelling – the next step in EITI reconciliations?

Knowing how to model a project’s revenue can strengthen the capacity of the government.

When the EITI set out its work ten years ago, the core idea was to reconcile and compare the payments made by companies and governments to each other to see if they added up to the same amount. This can and has uncovered problems such as corruption. In 2013 the Standard was expanded to cover the whole value chain including the legal, fiscal, licence and contractual terms and production data. This was a big leap, and gives stakeholders much more information. But the data still need extensive interpretation to become insight, or actual analysis.

Financial modelling, then, in the EITI context, could be thought of as “next level reconciliation.” Modelling goes a stage further than comparing figures: it analyses the terms of a contract, and the economics of the project, such as costs and real prices achieved. It then creates projections of what should have been paid by companies to the government under the existing agreement.

This is important because of information asymmetry: when one party has more or better information than the other during a negotiation.

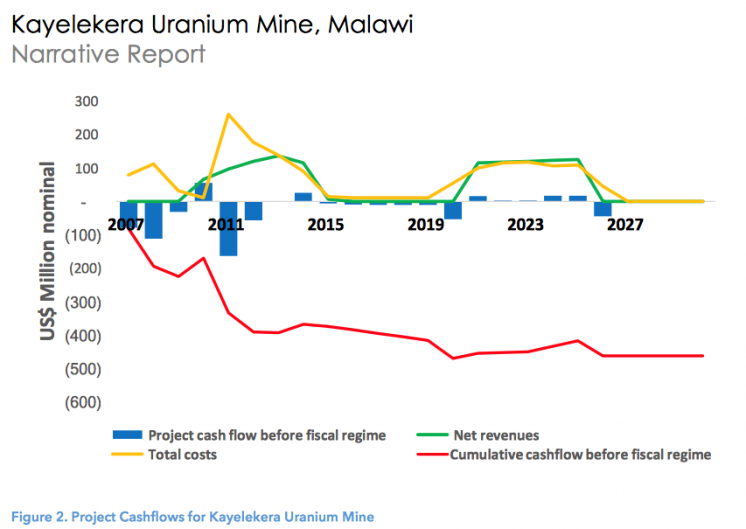

One output of the financial modelling: projection of cashflow from a uranium mine in Malawi (see more below). Source: Open Oil Report

A powerful tool

Contractual arrangements are often complex and subject to subtle interpretation of terms, and governments may not actually be able to tell precisely what they are owed. This is where financial modelling comes in.

Some revenue streams, like royalties, are in theory quite straightforward: take production, multiply it by the price, and then apply the royalty percentage rates to that “base”.

But revenue streams related to the profitability of the project – Corporate Income Tax, Resource Rent Tax, and so on – need more complex calculations. They involve the company's costs, terms of cost recovery, what are the “allowable costs”, and so on. There are too many disputes between companies and governments on these issues to safely say that this is an advanced technical area.

So a financial analysis which takes all these factors into account is not trivial. But without it, “real reconciliation” – is what has been paid what should have been paid – is just not possible. And that, after all, is the ultimate goal of much transparency work, including that of the EITI.

This explains the fast-growing interest in creating “public interest financial analysis”. And the early signs are that spreading modelling into the public space is possible.

Calculating when a mine can reopen, how many taxes are lost, and more

At OpenOil last year we invited teams that had spent months learning skills in Microsoft Excel and the basics of financial modelling, to complete models of significant projects in their country. The teams included civil society, researchers, and government representatives. All participants used the FAST modelling standard, which is widely used in the global financial services industry.

The results were highly encouraging. Six models were produced to “full fiscal level”, showing revenue predictions for the past (useful in tax gap analysis), forecasts for the future, and sensitivities to changing market conditions. Both government and civil society teams took part and spoke about their experiences.

To take a couple of examples from within EITI implementing countries: Mining in Malawi produced a model of Paladin’s uranium mine at Kayelekera, which showed that the government lost USD 15 million in revenues by agreeing to concessions on the royalty regime. The model also showed that the mine, which was closed in 2014 because of a crash in uranium prices, was unlikely to reopen, since the market price would need to more than double to make it viable – an issue of great public interest.

PWYP Indonesia produced a model of Batu Hijau gold mine, which showed that allowances for hedging losses in trading by the operator Newmont cost the government some USD 388 million in tax losses. Despite that, and a temporary closure in 2013-14, ongoing operation at the mine looked strongly profitable. The model also set up use of future EITI reconciliation data, since it will enable in this case analysis of how a new fiscal regime is playing out.

Once you start to reconcile what models predict with the actual payments recorded in EITI, reconciliations are mixed.

At Bulyanhulu in Tanzania, for example, royalty payments over the past few years closely match what the model predicts should have happened. But in Chad reconciliations do not show any royalties paid in the Mangara oil field whereas the model predicts tens of millions of dollars. And in Mali, while EITI Reports do show royalty payments for gold mines operated by RandGold, they are radically different to what the model (still in draft format) predicts based on company disclosures to its own investors, and in new disclosures under EU transparency rules.

Why you should learn financial modelling, and how

The point of financial modelling is to “follow the facts”. From a governance perspective, it is just as useful to find significant discrepancies, such as in Chad and Mali, as it is to find that calculated payments match the payments received, as in Tanzania.

These are early days. But the signs are that reliable public interest financial modelling can take hold in civil society as well as in government. This allows them to improve governance and manage expectations by reducing the information asymmetry and putting financial insight into the public sphere.

We invite anyone who is interested to sign up for a free online course in Excel, the “first rung” in the ladder of skillsets needed to get into financial analysis.

The author is director of OpenOil, a Berlin-based consultancy working for governments and civil society to increase insight into management of natural resources, and a friend of EITI since 2010.

Related content