Summary

With growing public attention on environmental issues, governments and companies are increasingly under pressure to monitor and mitigate environmental damage of human activities. This is particularly the case in the oil, gas and mining sector, which faces increasing scrutiny for its impact on the environment. The increasing demand for critical minerals is contributing footnote to further emphasis on mitigating the environmental impact of exploration and production.

Disclosures on environmental impact management and monitoring in the extractive industries can help citizens better understand the reforms and measures governments are taking to mitigate potentially negative environmental impacts. Such data is particularly relevant for communities affected by extractive operations.

Governments and oversight actors can use environmental disclosures to assess the adequacy of the regulatory framework, as well as management and monitoring efforts to mitigate the environmental impact of extractive industries.

By disclosing information on their environmental impact mitigation efforts, governments and companies can also demonstrate their efforts to protect the environment to the public, investors and local communities. Such data can further support assessments of extractive companies’ adherence to their environmental obligations.

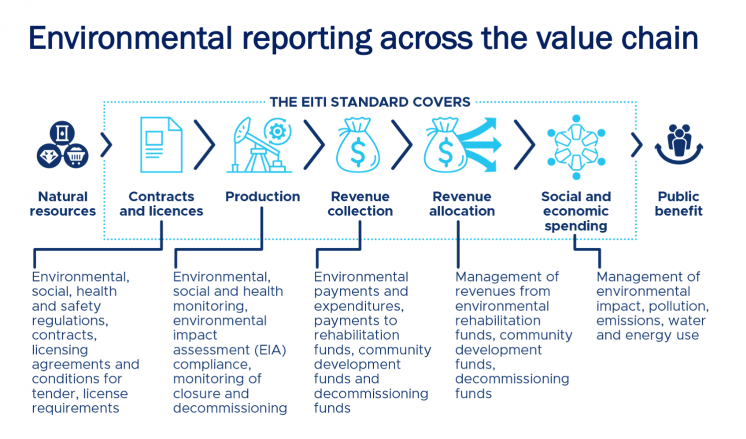

Requirement 6.4 of the EITI Standard encourages implementing countries to disclose information on the management and monitoring of the environmental impact of extractive activities. Stakeholders can agree areas of priority for disclosure, based on national priorities for the sector and demand for transparency at the national and local level. By including environmental disclosures in EITI reporting, stakeholders can better understand the regulatory framework and how it is implemented in practice.

This note provides step-by-step guidance to multi-stakeholder groups (MSGs) on how to disclose information related to management and monitoring of environmental impact, offers examples from implementing countries, and outlines opportunities to strengthen the dissemination and use of data.

- What are the existing environmental laws and regulations in the oil, gas and mining sector, and how are these enforced by relevant government agencies?

- How do oil, gas and mining companies report on their compliance to environmental regulations?

- Are there vulnerabilities, corruption or mismanagement risks in existing environmental management and monitoring systems?

Overview of steps

| steps | key considerations | examples |

|---|---|---|

|

Step 1: |

|

|

|

Step 2: |

|

|

|

Step 3: |

|

|

|

Step 4: |

|

|

How to implement Requirement 6.4

Step 1: Agree the objectives and scope of disclosures on environmental impact

MSGs are encouraged to agree objectives and activities that assist stakeholders in the assessment of:

- The adequacy of the regulatory framework as well as management and monitoring efforts

- Extractive companies’ adherence to environmental obligations

To inform this, the MSG is advised to consider:

- What is the demand for environmental impact information from different constituencies? Have stakeholders raised any concerns about the environmental management and monitoring? Are there national priorities that relate to environmental management and monitoring that the process can contribute to?

- Is the information about the applicable environmental regulatory framework available? Is it comprehensive and easy to understand?

- How are environmental regulations enforced? Which government agencies are responsible for environmental management and monitoring? Is the information on enforcement activities and results publicly available?

- How do companies inform stakeholders of their compliance with environmental regulations? Are there additional actions undertaken by companies to assess and mitigate their environmental impact? Is information about these actions publicly available?

- Are there any non-regulatory voluntary environmental standards, such as voluntary international sustainability reporting frameworks or guidance, that may be available at the national level?

- What other publicly available or potentially available information could be useful for managing and monitoring the environmental impact of extractive industries?

The specific objectives will vary from country to country. They will depend on national contexts, stakeholder interest and the availability, comprehensiveness and quality of the information. Examples of objectives could be:

- Strengthen government and industry procedures for management and monitoring of environmental impact and ensure a more effective environmental permit allocation process.

- Improve public understanding of environmental regulations and how they are enforced in practice.

- Improve public scrutiny of environmental management and monitoring activities and public understanding of corruption risks associated with enforcing environmental regulations.

- Improve industry environmental performance in accordance with the industry’s principles for environmental management.

The MSGs might also wish to identify where additional capacity building is needed to support the disclosure and analysis of information. The MSG might wish to consider whether such activities can be supported by MSG members or EITI stakeholders from various constituencies, or whether they would require engaging with specialists to strengthen capacity of key reporting agencies or stakeholders with an interest in using the information.

Albania and Uganda: EITI objectives and activities related to monitoring environmental impact

To monitor the negative environmental impacts of the petroleum industry, Albania EITI included activities in its work plan to assess technical processes, seismic oscillations, soil and water pollution and the impact of the industry on the lives of citizens living in proximity to extraction sites.

As part of Uganda EITI’s broader objective to strengthen revenue management and accountability, the MSG is planning activities aimed at monitoring compliance of the extractive sector with social and environmental regulations, frameworks and safeguards. It plans to produce policy papers with recommendations to improve compliance with social and environmental safeguards outlined in the environmental and social impact assessments.

Step 2: Identify existing disclosures by government agencies and companies

MSGs are advised to consider what information related to environmental impact is already disclosed, and how this data can be used and improved. In doing this, the MSG might address questions such as:

- Are the different components of the regulatory framework clearly identified and explained by key government agencies?

- Is the information on enforcement of environmental regulations available from relevant government agencies?

- Is this information comprehensive and publicly available?

- Are there gaps in information that need to be addressed? Are there gaps related to accessibility, timeliness, reliability and quality of information?

Government agencies and companies are likely to disclose different types of data with different levels of detail. Relevant government agencies can ensure that information is made accessible about the environmental management and monitoring framework that applies for all companies and projects.

Such information can be useful for companies to gain a clear understanding of what is expected from them and to ensure that they comply with the relevant regulations. This data can also provide context for company disclosures (e.g. data on water use disclosed by a company can be compared to data on water use at the industry-wide or regional level). Companies are often well placed to report more detailed information at the project level about measures to mitigate environmental impact.

Mexico: Identifying relevant regulations and disclosures on environmental information

In 2019, EITI Mexico commissioned a report on social and environmental aspects to be considered in the EITI disclosures. The report addresses regulations concerning forestry resources, water management, protective areas, maritime zones, residuals, environmental licenses, sanctions and insurance. It also describes regional funds dedicated to sustainable development and the programme by the state-owned company PEMEX for supporting community and environmental management (PACMA).

Latin America and the Caribbean: Analysis and recommendations from civil society on what to disclose

In 2016, the Latin American civil society network Red Latinoamericana sobre las Industrias Extractivas (RLIE) recommended a list of disclosures related to environmental management, including mining prospection studies, environmental impact assessments, mitigation plans, environmental liabilities funds and rehabilitation.

In Peru, civil society groups Derecho Ambiente y Recursos Naturales and Grupo Propuesta Ciudadana, which participate in Peru EITI’s MSG, published a study in 2019 on strengthening transparency of social and environmental information in EITI Peru and beyond.

The universe of information related to the management and monitoring of the environmental impact of extractive activities is vast. When identifying existing disclosures, the MSG could consider documenting the following types of information:

1. Disclosures that ensure transparency in how governments and companies manage environmental impact. These could include:

- Descriptions of existing legal provisions and administrative rules for managing environmental impact. This information can help stakeholders get a general overview of the relevant legal procedures and administrative rules and key actors involved, and can include:

- Laws, regulations and specific provisions related to the management of environmental impact of extractive industries.

- Relevant agencies, including their scope and roles and responsibilities.

Examples: Description of a legal environmental framework in the Kyrgyz Republic and Liberia and descriptions of agencies’ roles and responsibilities in Armenia, Colombia and Peru.

- Environmental management instruments such as environmental impact assessments (EIAs), certification schemes, licenses, rights or permits, etc. The IMF advises publication by the government of environmental and social impact assessments and associated management plans and reportsSee IMF (2019), IMF Fiscal Transparency Code, Dimension 4.4.4, p. 22.

- Descriptions or assessments of actual practice. These can help stakeholders understand how the framework is implemented in practice and what are possible areas of improvement. MSGs may include a description of the efforts made by the government to manage environmental impact of significant projects, an overview of EIAs undertaken, environmental certificates or licenses awarded, etc. If the supreme audit institution has undertaken environmental audits, these reports could help to understand how procedures are implemented in practice.

- Description of reforms that are planned or underway. If changes to existing regulations or practices are planned, the objective and timescale for such legislative changes could be outlined, including the process for stakeholder consultation.

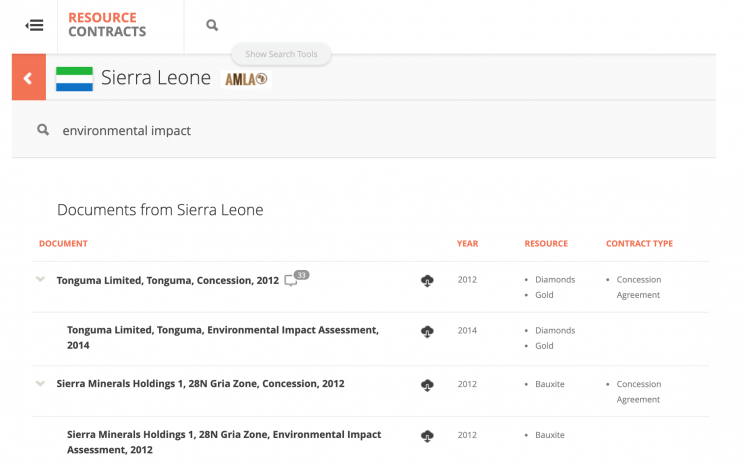

Sierra Leone and Peru: Enabling public access to environmental impact assessments (EIAs)

2. Disclosures that ensure transparency in how governments monitor environmental impacts. These could include:

- Descriptions of existing legal and administrative frameworks for monitoring environmental protection. This can help stakeholders get an overview of the relevant legal procedures and administrative rules and key actors involved, and can include:

- Laws, regulations and specific provisions related to monitoring environmental impact of extractive industries.

- Relevant agencies, including their scope and roles and responsibilities.

- Environmental monitoring instruments, such as sanctioning processes, environmental liabilities, rehabilitation and remediation programmes.

Examples: Disclosures on environmental certifications and sanctions in Peru and disclosures on environmental protection, rehabilitation and water and waste management in Mongolia.

- Descriptions or assessments of actual practices. MSGs could consider addressing aspects of these framework and actual practices on an ad hoc basis.

- Description of reforms that are planned or underway. If changes to existing regulations or practices are planned, the objective and timescale for such changes could be outlined, including the process for stakeholder consultation.

Mozambique: Results of audits to strengthen implementation of environmental legislation

Mozambique’s 2019 EITI Report highlights the environmental monitoring procedures and actual practice including an overview of environmental licenses awarded to companies. It also provides an overview of environmental audits undertaken by the National Agency for Environmental Quality Control. These audits covered the areas of waste management, effluent management, emissions management, biodiversity management, environmental rehabilitation, and risk management.

The report provides a summary of the main findings from the audits, including lack of compliance with the environmental legislation, companies operating without valid environmental licenses, poor implementation of the Environmental Management Plans and failure to implement measures to mitigate environmental quality standards among others. The report also highlights companies that produced environmental reports and the entities that prepared the reports.

3. Disclosures that help measure environmental impact of companies and projects. These could cover energy consumption, use of water, effluents and waste, efforts towards higher circularity, CO2 emissions, biodiversity, compliance with environmental laws and regulations and the number of environmental grievances filed.

Many companies disclose information on environmental management and impact through their sustainability reporting, applying standards such as the Global Reporting Initiative (GRI) Standards HideRelevant GRI Standards include “GRI 302 Energy”, “GRI 303 Water and Effluents”, “GRI 304 Biodiversity”, “GRI 305 Emissions” and “GRI 306 Waste”and the Sustainability Accounting Standards Board (SASB) StandardsHideSee the SASB Extractives & Minerals Processing Standards covering relevant subsectors such as coal, construction materials, iron and steel, metals & mining, oil and gas (exploration and production, midstream, refining & marketing and services). There is also sector-specific guidance such as the IPIECA sustainability reporting guidance for the oil and gas industry .

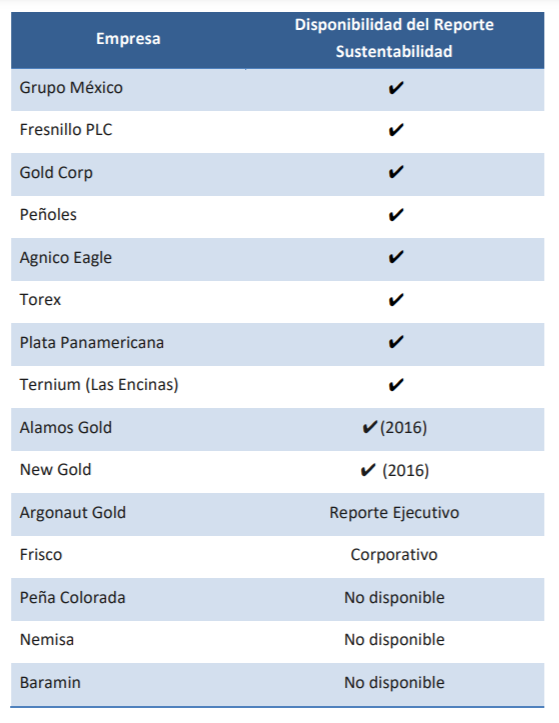

Mexico: Reviewing sustainability reporting by companies

In 2019, EITI Mexico conducted a scoping study which included a review of sustainability reports available for a sample of EITI reporting companies with an assessment on how many GRI indicators were reported.

Trinidad and Tobago: Improving access to emissions data for extractives projects

Trinidad and Tobago EITI (TTEITI) has been making efforts in improving the availability of data and increasing public awareness around climate change and energy transition. It has made efforts to focus reporting on the wider environmental and social impacts of the extractive industries including CO2 emissions.

TTEITI has established an environmental subcommittee with the responsibility of furthering work on environmental reporting. While there are no statutory systems for emissions monitoring in Trinidad and Tobago, a pilot programme has been implemented by the Ministry of Planning and Development for the monitoring and verification of emissions. TTEITI has developed a voluntary template for reporting resource impacts – including electricity, water usage, CO2 and methane – as well as statutory requirements related to air and water pollution. The subcommittee’s long-term aim is to move towards the incorporation of environmental and climate impacts in the sector, in conjunction with the Central Bank of Trinidad and Tobago and other agencies.

Step 3: Disclose information on environmental impact

Once the objectives and scope have been agreed, the MSG should establish how to disclose the necessary information. The MSG might wish to consider:

- Is there demand for any environmental management and monitoring information that is not publicly available?

- What is the best way to disclose or gather additional information? Could such information be systematically disclosed?

- How can environmental management and monitoring information be presented in a more accessible way (e.g., relevant website or portal, EITI reporting, thematic brief, special report, etc.)?

The MSG could consider a timetable for working with the relevant reporting entities to systematically disclose information on environmental impact and for disclosing information gaps through EITI reporting. The timetable should be aligned and integrated into the MSG’s annual work plan.

The MSG should consider the accessibility, inter-operability, comprehensiveness and quality of the information to be gathered or referenced. Information in open data formats should be prioritised. When information is not available and the MSG wishes to disclose data via other means, the MSG could consider synergies with other data collection systems such as company reporting portals or open data platforms.

The MSG could also consider the sustainability of these disclosures for subsequent reporting cycles, and design reporting frameworks that build on existing disclosure systems.

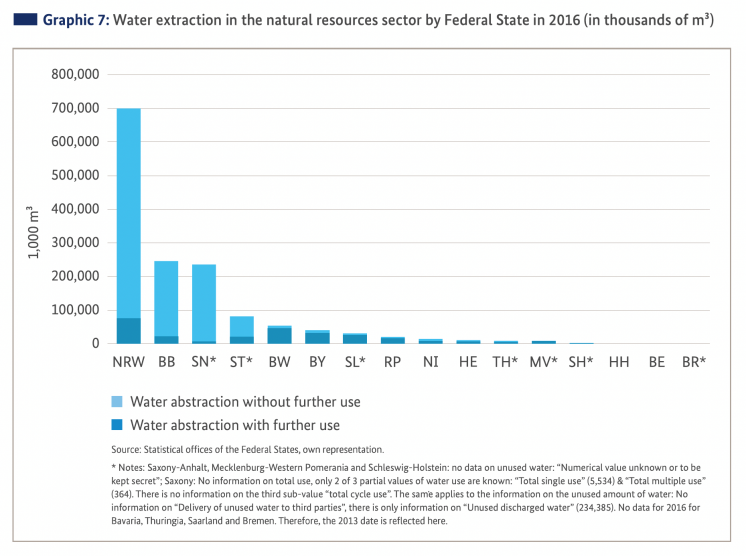

Germany: Monitoring water abstraction

The environmental impact of the mining sector is a challenging issue in some parts of Germany, where compensatory measures are legally regulated. Water extraction is a key feature of many mining projects.

Germany’s coal mining industry accounted for 5% of total water use by industry and private households in 2016 and has reached up to 30% in individual states. Most federal states levy consumption-related fees for the use of ground and surface water, which can act as incentives for sustainable water management programmes.

Germany has included water abstraction in its EITI reporting. Following an initiative by the Germany Multi-Stakeholder Group, an overview of fee levy rates was made publicly accessible on the government website, giving stakeholders greater oversight of the management of water resources.

Step 4: Review and analyse disclosures

The MSG is encouraged to review and analyse the disclosures, with a view to:

- Ensure that the disclosures are widely accessible and disseminated, and that they promote public debate on relevant issues related to environmental protection.

- Meet the objectives set for these disclosures. This could entail conducting an assessment of the adequacy of the regulatory framework, especially on the actual practices compared to the rules and procedures.

- Agree recommendations with a view to strengthen the impact of EITI implementation on natural resource governance. In particular, recommendations could address:

- Opportunities for improving systematic disclosures of data on environmental impact.

- How the information could be presented to help stakeholders better understand the regulatory framework and its enforcement.

- Identify corruption risks associated with applying this regulatory framework and suggest actions for mitigating these risksHideExisting research on corruption in environmental management can support MSGs in identifying risk areas. Examples: OECD (2016), Corruption in the Extractive Value Chain (see sections on “Specific risk factors associated with environmental and social impact assessments and land tenure” and “Corruption in relation with violation of environmental regulations”), and U4 (2016), Deciding over nature: Corruption and environmental impact assessments.

The MSG might wish to consider the following questions:

- What additional analysis should be undertaken to respond to the objectives agreed in Step 1?

- What is the best way to review and discuss the information disclosed or referenced on the managing and monitoring of the environmental impact of extractive industries?

- What is the best way to document the review and analysis of the information presented as part of this requirement?

- Is there a need to expand the initially agreed scope of disclosures?

The Philippines: Recommendations to disclose details on environmental permits and rehabilitation activities

In addition to including information on protection and rehabilitation funds, the Philippines' 2018 EITI Report presents several recommendations for improving transparency of environmental expenditures, impact assessments and environmental management. For instance, the report proposes that information on auxiliary rights (e.g. water rights, tree cutting permits) given to extractive companies should be disclosed, and that companies should disclose and provide updates on its rehabilitation activities (i.e. affected land area, rehabilitated lands, efforts on recovering the natural ecosystem).

The Democratic Republic of the Congo: Recommendations to disclose environmental impact assessments (EIAs)

The DRC’s 2018-2020 EITI Report includes detailed information on the roles of different agencies in monitoring the impact of extractives, such as the Congolese Environmental Agency (ACE). It highlights the importance of disclosing further information to allow local communities and civil society to understand companies’ obligations and government agencies’ oversight of the latter.

The report recommends that the Ministry of Mines, the Ministry of Hydrocarbons and extractive companies publish summaries of the EIAs completed as part of the license award process. It also recommends that the Ministry of Environment publish reports on its follow-up on mining operators’ environmental obligations.

Dissemination and use of data

Environmental reporting can promote public understanding, debate and reform. To harness the benefits of such disclosures, the MSG should endeavour to communicate disclosures to citizens and relevant stakeholders. To this end, the MSG can consider conducting capacity building activities to make sure that citizens and stakeholders understand environmental disclosures and how they can be analysed and used.

Ukraine: Local forums on environmental impact and protection

Ukraine EITI hosts between 50 and 70 local events per year to communicate the findings of EITI reporting, such as impacts of extraction and revenue allocations that local communities receive. For some of these events, discussions have focused on environmental impact and protection.

These forums have been a useful platform for citizens, industry and government representatives to debate and resolve environmental issues, as well as other matters pertaining to natural resource management.

Further resources

- Chatham House (2020), Transparency in Transition.

- EITI (2021), Guidance on EITI Requirement 6.1: Social and environmental expenditures.

- EITI (2017), Coverage of environmental information in EITI reporting.

- IPIECA (2020), Sustainability reporting guidance for the oil and gas industry.

- Natural Resource Governance Institute (2019), Beyond Revenues: Measuring and Valuing Environmental and Social Impacts in Extractive Sector Governance.

- Sustainability Accounting Standards Board (2018), SASB Extractives & Minerals Processing Standards.

- UNEP (2020), Sustainability in the Mining Sector: Current Status and Future Trends.

- World Bank (2018), Environmental and Social Framework.