Summary

Prices for natural resources such as oil, gas and precious metals are subject to volatility, making the returns on these resources difficult to estimate. Major events that affect the global economy, such as the 2008 financial crisis, the 2014 oil crash and the COVID-19 pandemic, have caused sharp decreases in oil prices that negatively affected many hydrocarbon-producing countries. Furthermore, conflicts and wars such as the conflict in Ukraine have also led to sharp increases in oil prices, thrusting the issue of energy security into sharp relief in many parts of the world. Looking ahead, the global shift to a low-carbon economy may bring risks and opportunities for countries that develop fossil fuels, transition minerals, renewable energies and carbon sinks. While the extractive and energy sectors are likely to evolve, it is difficult to predict how and when demand trajectories and investment trends will change.

In this context of high uncertainty, it is important that resource-rich countries understand the factors that affect revenues from the extractive sector. Preparing for price shocks and market evolutions by, for example, developing forward-looking plans and budgets under different price scenarios, is essential for managing extractive revenues sustainably. Revenue sustainability is key for mitigating the negative impacts of economic downturns and avoiding the “resource curse”, where countries could experience short-term gains and long-term fiscal distress.

Good governance of the extractive sector requires sound forecasting and management of the different risks and opportunities. By adopting a forward-looking approach, governments are better placed to optimise future revenues and anticipate necessary investments, as well as inform debate on how extraction will benefit citizens in the future. This is particularly relevant for highly indebted countries that rely on future revenues to cover their debt repayments and maintain their creditworthiness. Finally, data-driven forecasting can help countries prepare for the economic impacts of the energy transition.

The EITI offers a platform for debate on this topic based on data and quantitative analysis. Requirement 5.3.c of the EITI Standard encourages timely information to strengthen public understanding and debate around issues of revenue sustainability and resource dependence. Whereas EITI reporting traditionally focuses on disclosure and reconciliation of past payments and revenues in the extractive sector, this provision encourages countries to consider the sustainability of revenues in the context of different market scenarios.

This note offers step-by-step guidance to multi-stakeholder groups (MSGs) on using EITI implementation to conduct forward-looking analysis on revenue sustainability. It outlines some of the risks and opportunities for future revenue generation that MSGs may wish to consider, including factors pertaining to the energy transition. It also guides MSGs on the different factors and assumptions they could consider when undertaking forecast exercises. Finally, this note highlights some of the common challenges in sustainable revenue management and measures to mitigate these, as well as opportunities for leveraging alternative approaches to EITI reporting to support MSGs’ work in this area.

Overview of steps

| Steps | key considerations | examples |

|---|---|---|

|

Step 1: |

|

|

|

Step 2: |

|

|

|

Step 3: |

|

|

|

Step 4: |

|

|

|

Step 5: |

|

|

How to implement Requirement 5.3.c

Step 1: Identify risks and opportunities for future revenues

To contribute to debate and decision-making on sustainable revenue management, MSGs could undertake a risk-based and forward-looking analysis. EITI Reports provide a credible and rich source of information on government revenues, which can provide a broader understanding of the economic contribution of the extractive industries and a country’s dependence on the sector. MSGs could seek to identify the short-term and long-term risks and opportunities for future extractive revenue streams in order to help governments prepare for different scenarios and inform policymaking on sustainable debt management.

Furthermore, while maximising revenues from natural resources is a major objective for many implementing countries, this can be a challenge given the inherent volatility of prices and demand for oil, gas and minerals. By discussing the risks and opportunities for future revenues, MSGs can shed light on the parameters affecting future income and inform national budget assumptions. To inform its discussion on revenue sustainability, MSGs could consider the following:

- Assess the future of the extractive sector in the country. As a starting point, MSGs can assess the general outlook of the country’s extractive sector. This can include a review of past and current dependence on the extractive sector, projected contribution of the sector to the economy, investment inflows into the sector and the stage of development for large extractive projects. The MSG can also review existing revenue forecasts (including the assumptions underpinning these) as well as high-level economic outlooks and global market trends.

- Map and debate potential risks and opportunities that may affect revenue sustainability. Countries may be exposed to disadvantageous and/or favourable scenarios which could potentially decrease or increase revenue flows. MSGs are encouraged to consider such risks and opportunities in order to inform planning around revenue management. MSGs could consider the following risks and opportunities:

Risks:

- Sudden, rapid decrease of prices and demand for a commodity which the country produces.

- Slow, long-term decline of prices and demand for a commodity which the country produces.

- Structural decline of production or aging of production infrastructures.

- Inadequacies of the fiscal regime to respond to price or production shocks.

- Competition from other producing countries better positioned to attract investment and generate returns.

- Insufficient revenues and lack of long-term savings after fulfilling commitments to reimburse costs or resource-backed loans.

- Major project delays that impact the timing of revenue flows.

Opportunities:

- Sudden, rapid increase of prices and demand for a commodity which the country produces or could potentially produce.

- Long-term increase of prices and demand for a commodity which the country produces or could develop by making the necessary investments and policy reforms.

- Ability of the legal and fiscal regime to attract investors.

MSGs may also consider other scenarios relevant to the country.

- Consider risks and opportunities associated to the energy transition. The term “energy transition” commonly refers to the process whereby the world economy is transitioning towards a low-carbon economy. While access to energy is crucial for the world’s growing population, climate change, energy security considerations, geopolitics and technology are also driving changes in the demand and supply of energy. The short-term and long-term outlooks for the energy sector are highly uncertain, as is the timing of future changes. There are multiple scenarios as a result of country and energy producers’ commitments to achieve carbon neutrality by 2050.

Good governance of the extractive sector thus implies good management of both short-term and long-term risks and opportunities associated with the different global market scenarios. MSGs are encouraged to debate the major risks and opportunities associated with the energy transition that will affect government revenues from the extractive sector. MSGs could consider the following:

Risk and opportunities for fossil fuels:

- A decline in coal and hydrocarbon prices could have an impact on profitability of some projects and lead to revenue loss. Some projects may become unprofitable and become stranded assets.

- A decline of investments in fossil fuel exploration and development could lead to revenue loss, requiring oil-dependent countries to diversify their economies.

- Costly and high breakeven projects could be at risk of being terminated by investors.

- Increased demand of transition fuels, such as gas and liquefied natural gas (LNG), could provide an opportunity for stopping flaring and monetising gas reserves that were previously unprofitable.

- Low-cost and breakeven projects could provide an opportunity for countries to remain competitive.

Risk and opportunities for critical minerals:

- A potential increase of demand and prices for transition minerals (e.g. cobalt, copper or lithium) could provide an opportunity to attract additional investment and revenues.

- Entering deals in which a commodity is misevaluated or undervalued could lead to revenue loss for the state.

- Non-competitive fiscal regimes or infrastructures, as well as governance challenges or poor reputation, could drive away investors.

Risk and opportunities for renewables and carbon sinks:

- The ESG investment boom could attract additional financing in, and revenues from, renewable energy projects.

- The ESG investment boom could attract additional financing in, and revenues from, carbon sink projects (e.g. forestation, carbon capture and storage).

- Coupling extractive projects with renewable and carbon sink projects could provide an opportunity to improve ESG competitiveness.

- Entering deals in which a commodity is misevaluated or undervalued could lead to revenue loss for the state.

- Non-competitive fiscal regimes or infrastructures, as well as governance challenges or poor reputation, could drive away investors.

- Consider exposure to debt. An analysis of the sustainability of the revenues is especially relevant for countries with heavy debt exposure. In these countries, both governments and lenders – such as the IMF, private creditors and ratings agencies – have an interest in understanding the outlook for future revenues and the reliability of economic projections according to different scenarios. Transparency can help improve the country’s reliability profile and creditworthiness, and revenue forecasting can help to assess the ability of a country to meet its reimbursement commitments.

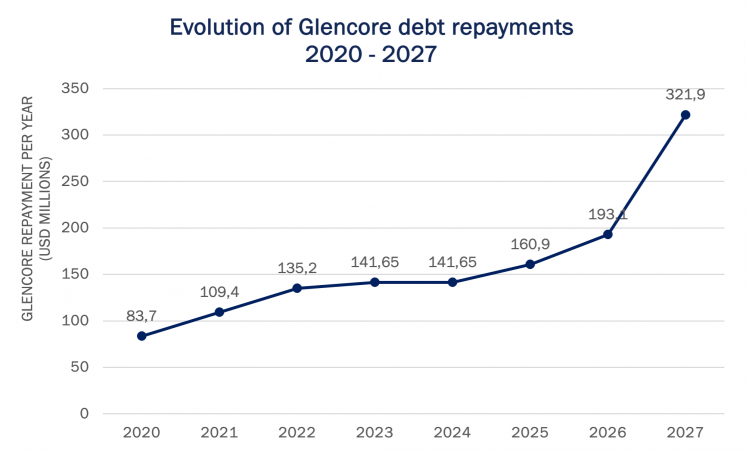

Chad: Understanding debt commitments with disclosure of resource-backed loans

In 2013 and 2014, Chad’s national oil company, SHT, contracted two loans on behalf of the Chadian state worth USD 0.6 billion and USD 1.45 billion respectively. The loans were granted by Glencore Energy UK and supported by a consortium of banks. According to the contracts, repayments were to be made through direct deductions from oil shipments sold by the commodity trading company Glencore. In 2015 and 2018, the debts were restructured in order to counteract the oil price crash and alleviate the debt, which had become unsustainable.

Since 2018, key terms of these pre-financing contracts have been made public through EITI reporting. According to Chad’s 2019 EITI Report, a debt principal of USD 1.28 billion was to be reimbursed in 2019 (with maturity up to 2027), representing 11.7% of the country’s GDP.

Step 2: Determine priorities and disclosure objectives

Before conducting an analysis on future revenues, the MSG should first agree key objectives that will help inform debate on revenue sustainability. For example, the MSG could consider one or more of the following:

- Mapping the risks and opportunities that will affect future revenues from the extractive sector.

- Understanding revenue resilience to price shocks.

- Understanding the revenue split between companies and government at different stages of a project.

- Understanding the risks and opportunities for future revenues associated with market evolutions and the energy transition.

- Understanding the vulnerability of a project in relation to particular fiscal or economic parameters.

In agreeing objectives, the MSG should also determine the timeframe that their analysis should cover in order to answer key questions on the sustainability of the country’s future extractive revenues. The analysis could cover short-term future years (e.g. 1-5 years), long-term future years (e.g. covering the life expectancy of the assets) and/or historical data.

Nigeria: Economic exposure to energy transition

Nigeria derives about 65% of government revenue and about 90% of foreign exchange earnings from the sale of crude oil. As the energy transition gathers pace, the prospects for shifting demand for fossil fuels portends far-reaching implications for Nigeria’s economy. Reports by Nigeria EITI (NEITI) have sought to highlight the impact of large fossil fuel subsidies on government revenues over the years. Nigeria’s 2020 EITI Report recommended that the government should “fully deregulate the downstream sector and savings made from the stoppage of the subsidy regime should be used to improve the life of citizens.”

Furthermore, a NEITI study is underway to better understand the potential impact of energy transition on Nigeria’s oil and gas sector. The study will analyse production and revenue data derived from EITI reporting in order to forecast the potential impacts and risks of the energy transition on government revenue and expenditure (including the potential for stranded assets, divestments or bankruptcies). Furthermore, the study will assess the extent to which existing legal, regulatory and contractual frameworks are relevant for Nigeria’s climate change mitigation and adaptation commitments and the energy transition more generally. The findings are expected to help inform public debate around issues of revenue sustainability and resource dependence, and to provide a basis for embedding energy transition monitoring in NEITI’s reporting processes.

Indonesia: Assessing the economic impact of the energy transition on critical minerals sector

Indonesia is rich in mineral deposits and is the largest producer of nickel globally. According to its national strategy, the country aims to become a global leader in the battery industry and to increase investments and revenues from critical minerals by strengthening its regulatory framework. In an effort to support the Indonesian government in developing regulations for its critical minerals sector, the EITI International Secretariat is carrying out a study on the governance risks for the country’s critical mineral supply chains, specifically for battery minerals such as nickel, cobalt, aluminium, manganese and tin. The study, which is comprised of a desk review and consultations with key stakeholders and experts, aims to provide recommendations and risk mitigation measures to help improve governance of the sector.

Step 3: Determine and collect the data needed

A good understanding of estimated future revenues, as well as the different scenarios and assumptions underpinning these revenue projections, can inform decision-making on revenue optimisation and sustainability. Several factors can affect future revenues, including the fiscal regime and contractual key terms, expected production and costs, sale, fiscal prices and reimbursement commitments. If the parameters affecting future revenues and their impacts are understood, countries can be more agile in making the necessary adjustments to optimise their revenues. To undertake this type of analysis, the MSG could consider the following steps:

- List the data already available. MSGs could consider the level of revenue forecasting already available. Is there any existing information related to the budget cycle, production and commodity price assumptions, estimated costs, resource dependence or revenue forecasting? If yes, where and how is this information disclosed? Is it available through government and company platforms or through EITI reporting?

When identifying existing data that is needed to support analysis on revenue sustainability, MSGs could consider the following data points:

- Expected revenues

- Future production levels

- Future costs (investments costs and production costs) and expected cost recovery

- Sales price assumptions and fiscal price assumptions

- Terms and conditions of extractive contracts

- Terms and conditions of resource-backed loans

- Outstanding debt levels

- Budget assumptions on the above parameters and scenarios used for budget elaboration

- Existing analyses on the sensitivity of revenues to the above parameters

- Assumptions of future market outlooks underpinning decision-making (e.g. supply, demand, prices)

- Determine the type of analysis needed and data gaps. Depending on the objectives listed in Step 2 and the level of data already available, the MSG should agree the type of analysis that is needed.

For example, the MSG may want to pursue a light, back-of-the-envelope overview of revenue sustainability and resilience. Alternatively, the MSG could undertake a more comprehensive quantitative analysis of financial projections using financial modelling.

If the MSG determines that a thorough quantitative analysis is needed, it should consider factors related to the national contractual frameworks and specific extractive projects. Data on the key contractual terms, as well as projections of future production levels, future costs and cost recovery, assumptions of fiscal prices and selling prices, will be particularly relevant for this type of analysis.

If further data is needed to undertake an analysis, the MSG could seek to map data gaps and identify potential sources for obtaining this data. - Consider data on the impact of the energy transition. MSGs are encouraged to consider the impact of the energy transition on demand trajectories and investment trends, and the implications these may have on future revenues. To this end, MSGs could consider the following data points when undertaking forward-looking analysis:

Data related to revenue dependence and energy transition scenarios:

- Expected share of the extractive sector in the economy and revenue dependence to extractives.

- Assumptions of future market outlooks and scenarios used in decision-making and budget elaboration (e.g. supply, demand, prices).

- Expected long-term production, investments and cost levels.

- Different price scenarios (e.g. the International Energy Agency’s sustainable development scenarioHideThe International Energy Agency’s sustainable development scenario is based on a “well below 2 °C” pathway under the Paris Agreement. For more information, see IEA (no date), Sustainable Development Scenario (SDS). or scenarios defined in cooperation with companies, government, civil society and international partners).

- Expected CO2 emissions from extractive production.

Data related to profitability of assets:

- Benchmarking of cost levels, shut-in prices and breakeven prices (i.e. the sales price at which a project is profitable).

- Assessments of the country’s risk of stranded assets at certain prices (i.e. prices at which assets cannot be developed profitably).

- Estimated reserves.

Data related to diversification opportunities:

- Analysis of the competitiveness of the country in relation to fossil fuel investments, critical minerals, renewables and carbon sink projects.

- Current levels of gas flaring and the country’s potential in developing gas and LNG as a transition fuel, and infrastructure needed to develop these.

- The country’s potential in developing critical minerals and infrastructure needed to develop these.

- The country’s potential in developing renewables and natural carbon sinks and infrastructure needed to develop these.

Depending on the complexity and depth of the analysis, the MSG may want to understand the quantitative impacts using financial modelling of past and future revenues, highlighting the potential impact of energy transition. This could require detailed forward-looking data as described in Step 1, disaggregated by year and project in line with the relevant contractual and fiscal framework. Other data or disaggregation may be needed depending on the contractual and fiscal framework.

Mauritania: Impact of energy transition on offshore gas and green hydrogen revenues

Mauritania is at the forefront of the energy transition thanks to the revenue prospects associated with major energy projects. The discovery of liquefied natural gas (LNG) off the coasts of Senegal and Mauritania offers the prospect of revenue from the exploitation of the main offshore gas field, Grand Tortue Ahmeyim (GTA). Mauritania is also committed to increasing the share of renewable energy in its energy mix to 60% by 2030 and has a strong solar, wind and hydro potential. It has signed two memoranda of understanding for large-scale green hydrogen production.

A study is underway to assess the impact of the energy transition on government revenues, based on data reported under the EITI Standard. The study will address the impact on revenues from both the oil and gas sector and the green hydrogen sector. The analysis is supported by systematic disclosures and data from EITI Reports (e.g. on the fiscal framework), as well as data provided by the Mauritanian government or contained in public contracts (e.g. investment costs, production estimates and operating costs).

The study will present financial models to estimate total government revenues over the estimated life of the projects involved. The model will include alternative scenarios based on gas prices and annual production volumes.

4. Identify entities which can provide missing data. The required data may be scattered across different sources. The MSG should consider which entities could provide the data (e.g. specific ministries). To link with budget processes, the MSG may also wish to request the budget assumptions from the government. Some data may also be provided by companies, who may have their own projections and analysis of revenue sustainability.

Step 4: Analyse the data

Once data is collected, the MSG should consider whether it provides answers to the questions and objectives determined in Step 2, as well as the general objective of Requirement 5.3.c. For instance, the MSG could reflect on the following questions:

- Does the data provide information about future risks and opportunities for revenues?

- Does the data provide information about the level of resource dependence?

- What is the sector’s exposure to low prices? To high prices?

- How sensitive are revenues to key parameters (e.g. price, production, costs, etc.)?

- Is there enough information to forecast the level and proportion of fiscal revenues expected to come from the extractive sector?

- Is financial modelling needed to better understand the forecasts?

Depending on the answers and on the complexity of the analysis needed, the MSG may want to gain an understanding of the quantitative impacts by using financial modelling of past and future revenues, highlighting the key risk parameters for revenue sustainability. This type of analysis could require that the data is disaggregated per year and at project level in line with the relevant contractual and fiscal frameworks.

If financial modelling is needed, the MSG should consider whether there is capacity within the government to undertake this type of analysis, or whether to engage an external partner to conduct the analysis and provide recommendations.

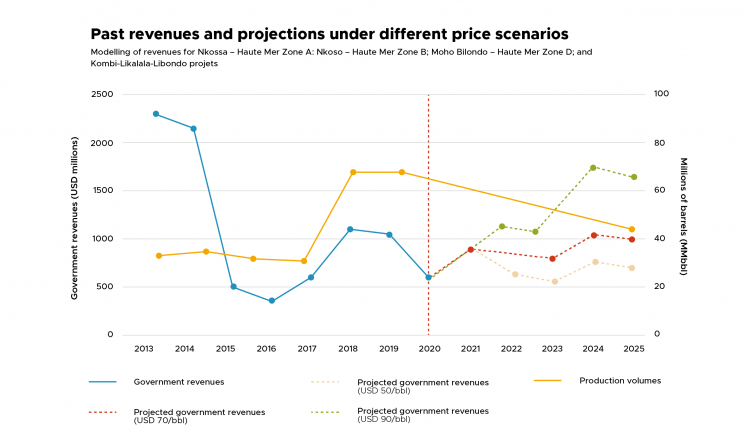

Republic of the Congo: Modelling past and future revenues to identify opportunities for revenue maximisation

As one of the largest oil producers in Africa, the Republic of the Congo generates nearly 98% of its total extractive revenues from the petroleum sector. The sustainability of these revenues is a key question for the country’s long-term economic health. Building on existing disclosures, the EITI in the Republic of the Congo launched a financial modelling project to examine past trends and future scenarios pertaining to the state’s share of oil revenues, from the point of extraction to sales on the international market.

The analysis draws on project-level data disclosed through EITI reporting to examine key parameters that affected revenues in four major oil fields between 2013 and 2020, a period marked by sudden decrease of oil prices. It also estimates future revenues until 2025 under different price scenarios.

In addition, the analysis examines EITI disclosures on oil sales by cargo for all companies operating in the country to identify potential vulnerabilities for future revenues at the sales level and the fiscal price methodology. The report also includes a section on costs, and observations pertaining to the performance of the tax regime.

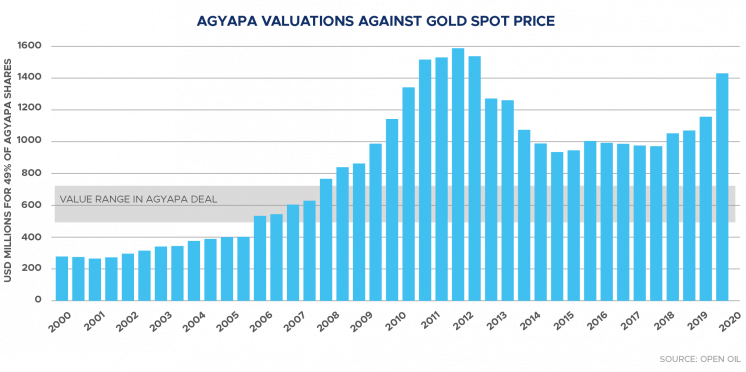

Ghana: Using EITI data to conduct valuation modelling and inform fiscal policies

In August 2020, Ghana's parliament approved a bill allowing the government to invest mineral royalties in a special purpose vehicle called Agyapa Royalty Limited, and to issue 49% of the company’s shares to public investors. The deal was established to secure short term capital (USD 500 million) to finance development priorities. Civil society stakeholders expressed concerns about the deal, particularly the basis for valuing Agyapa at USD 1 billion and the future fiscal implications of the agreement.

The question of whether the transaction presented a fair value for the country was a matter of public interest. To inform debate on this issue, data from Ghana’s EITI reporting was used to undertake a valuation modelling study. Production data was used to estimate future production from mines whose royalties would flow to Agyapa. Together with other assumptions (e.g. gold price, royalty rates and relevant mines), information from EITI reporting and other sources were used to estimate the value of Agyapa. The analysis concluded that the 49% of Agyapa shares – assessed by the government at a value of between USD 500 million and USD 750 million – appeared to be undervalued.

The findings and recommendations from the report informed public debate on the government’s policy in addressing short-term revenue needs against long-term debt and revenue sustainability imperatives. The government subsequently suspended finalising the deal to conduct further consultation with stakeholders.

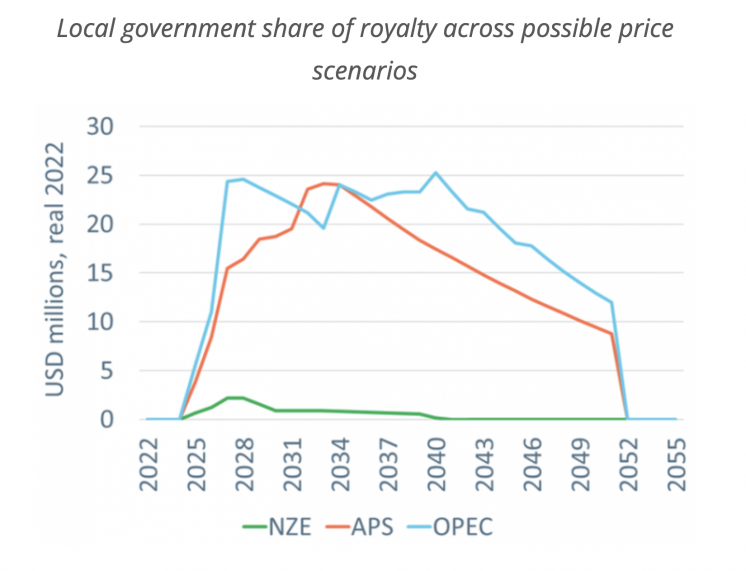

Uganda: Estimating oil revenue shares to local governments under different demand scenarios

Uganda’s USD 1.4 billion Lake Albert project is planned to begin oil production in 2025. However, the amount of revenue that both the central government and local governments will receive from the project remains unclear in view of possible oil price volatility and shifts in demand brought about by the energy transition.

To bring greater clarity and inform debate on expected revenues that local governments can expect, the Natural Resource Governance Institute (NRGI) developed a model that estimates royalty shares over the coming decades. The analysis considers potential revenues across three global demand scenarios:

- The Announced Pledges Scenario (APS) from the International Energy Agency (IEA), which assumes that countries implement their climate commitments;

- The reference scenario of the Organization of the Petroleum Exporting Countries (OPEC), which envisages a slower transition;

- The Net Zero (NZE) scenario from the IEA, which assumes a faster transition to net zero emissions by 2050.

The analysis demonstrates that local government revenues differ significantly between these scenarios. Uganda’s local governments could receive around USD 20 million a year on average under the OPEC scenario. By contrast, the NZE scenario predicts local revenues would amount to around USD 0.6 million. Greater clarity on the revenue sharing mechanism is needed to enable more detailed analysis and forecasting. To this end, the EITI offers a platform to spur debate, government action and disclosure of the revenue sharing formula and subnational revenue allocations to regions impacted by oil production activities.

Step 5: Disseminate findings

MSGs are encouraged to disseminate their findings to relevant entities to promote debate on the opportunities and risks related to revenue sustainability and inform evidence-based policymaking. Once the analysis is concluded, the MSG may wish to formulate concrete recommendations for the government and other stakeholders to consider, for example on strengthening the fiscal framework or improving revenue allocation systems.

Finally, in order to promote public debate, the MSG could consider presenting the findings and recommendations in a manner that is accessible and engaging for key audiences, for example by providing a summary report or disseminating data via relevant channels and/or in the local language(s).

Zambia: Reviewing the sustainability of fiscal regime with financial modelling

Zambia has changed its fiscal regime several times in an effort to attract investment while maximising government revenue. In 2019, the government proposed changes that included an increase in taxes charged on copper. Subsequently, Zambia EITI (ZEITI) commissioned a study to assess whether the proposed taxation regime negatively affected the performance of the mining companies. This included an analysis of companies’ forecast financials and their historical performance.

The study assessed the average returns for Zambian mining companies under the existing fiscal regime and under different price scenarios. ZEITI also assessed the historical tax rate for Zambian copper mining companies and how this rate compared with other copper mining jurisdictions such as Australia, Chile and Peru.

The findings were presented at a national, government-led multi-stakeholder meeting in 2021 and were coupled with training for government officials on analysis of financial models. These efforts have since contributed to public debate on the need to for an evidence-based design of an optimal fiscal regime. They have also drawn attention to the need to monitor production costs and improved the capacity of government officers in reviewing the financial models and financial statements from companies.

Mozambique: Understanding state loan guarantees and debt exposure

In 2018, the Mozambican government published a report on projected government revenues from gas projects. The report noted that, as a project concessionaire, the state-owned enterprise (SOE) ENH would not generate dividends for the government during the first years of the projects. Revenues from the gas projects would serve primarily to reimburse the company’s debt in relation to the equity financing during the exploration and construction phase.

Furthermore, Mozambique EITI published a separate report on SOEs’ participation in the extractive sector. The report aimed in part at determining ENH’s debt exposure and the potential impact of this debt on government gas revenues. It estimated ENH’s debt exposure to amount to almost USD 6 billion for its participation in the gas projects. The government subsequently had to issue a guarantee of USD 2.2 billion, included in the 2019 state budget. The report recommended that ENH and the government publicly disclose information on the loan guarantee, including the interest rate and payment schedule, in-order to enable analysis on the state and the SOE’s full debt exposure.

Common challenges in implementing Requirement 5.3.c

| possible challenges | response |

|---|---|

| MSGs may not see the analysis of revenue sustainability as being part of their role or of the EITI’s mandate more generally. |

According to the EITI Principles, “the prudent use of natural resource wealth should be an important engine for sustainable economic growth that contributes to sustainable development and poverty reduction, but if not managed properly, can create negative economic and social impacts.” In this spirit, MSGs can have an important role to play in promoting good governance by identifying the risks and opportunities for future income from the extractive sector, with the aim of optimising revenues and ensuring sustainable management of debt. This guidance note provides lists of short-term and long-term risks and opportunities related to the extractive sector. |

| The energy transition is not a policy priority for the government or the MSG. |

The energy transition may bring risks and opportunities for resource-rich countries. While the EITI does not advise governments on specific energy transition policies, it can support resource-rich countries in identifying and addressing the economic implications of the transition. Analysis of data reported through the EITI can help governments and citizens forecast how their economies may be impacted in the coming decades. |

| The data needed to undertake an analysis of revenue sustainability is not required by the EITI Standard, and is therefore not available. |

MSGs can play an active role in seeking the data that is needed to undertake an analysis on revenue sustainability (e.g. forward-looking and disaggregated data). The MSG could engage specific ministries and companies to obtain this data. |

| MSGs and stakeholders have limited resources and technical capacity to analyse data linked to revenue sustainability. |

MSGs can engage consultants and experts to undertake more complex analyses such as financial modelling. When developing Terms of Reference for consultants, MSGs could consider specifying project deliverables such as a summary report, key recommendations, visual material and/or capacity-building sessions. |

| The data needed to undertake an analysis on revenue sustainability may be confidential. |

While the EITI promotes transparency and accountability across all aspects of the upstream extractive sector, the MSG may consider signing non-disclosure agreements as a first step while the analysis is performed, if necessary. |

Leveraging alternative approaches to reporting

Traditional EITI reporting involves reconciliation of company payments and government revenues, which focuses on historical data. However, analysing the sustainability of revenues from the extractive sector requires a forward-looking approach that goes beyond reconciliation. In 2020, in response to the COVID-19 pandemic, the EITI Board introduced alternative approaches to reporting by providing countries with more flexibility to adapt their reporting to local circumstances and urgent information needs. It also introduced a pilot project, enabling select MSGs to deviate from conventional reporting procedures and to expand their role to undertake data analysis.

By adopting a flexible approach, some MSGs have been able to free up resources and publish thematic reports in addition to the EITI Report, for example on beneficial ownership disclosure, revenue allocations and gaps in SOE management. In the same spirit, MSGs are encouraged to consider publishing a specific report on revenue sustainability, or to integrate their analysis as a dedicated section in their EITI Report.